Decentralized Microfinance

Decentralized Microfinance

How DeFi can be leveraged to support inclusive financial services.

2020 was arguably the most turbulent year in modern history, with the COVID-19 pandemic claiming over 2.06M lives (at the time of this writing) and much of the world falling into a dystopian, socially distanced, and economically recessed reality. Despite many of the drawbacks of the pandemic, its socioeconomic effects have revealed several weaknesses in how governments and nonprofits respond to global crisis and mobilize to protect those most in need — One of the most notable of these frailties is the lack of modernized systems to scale social protection delivery to already struggling communities grappling with food and housing insecurity.

During this same time, the potential of decentralized finance (DeFi) has exploded. As of 2021, there is $23.31B locked within DeFi protocols globally, and new platforms are being released everyday. Consumers can now trade cryptocurrency futures, options, synthetic tokens, interest bearing tokens, and even take out loans — all without the need for a bank. BTC nearly reached an all time high of $41k, and major financial institutions have begun to crowd the crypto space to provide new products to their retail and high net-worth investors, purchasing over $600M in BTC alone. In response, regulators have sprung into action

However, many of these use cases don’t really help those in need — and, arguably, neither does BTC in any sustainable way. Transaction costs on the Bitcoin, and now even the Ethereum blockchains are simply too high to build applications (dApps) that can scale, and the user experience of many dApps still have extremely poor user experience design. In fact, I’d go as far as to say that most of the blockchain ecosystem’s products are just as unusable to mainstream consumers as it was in 2017, with maybe the exception to the use of stable-coins like USDC. The vast majority of DeFi protocol users are crypto-literate technophiles and speculative investors — not the 2B workers in the Informal Economy that have little to no access to financial services around the world.

An Introduction to Centrifuge and Tinlake

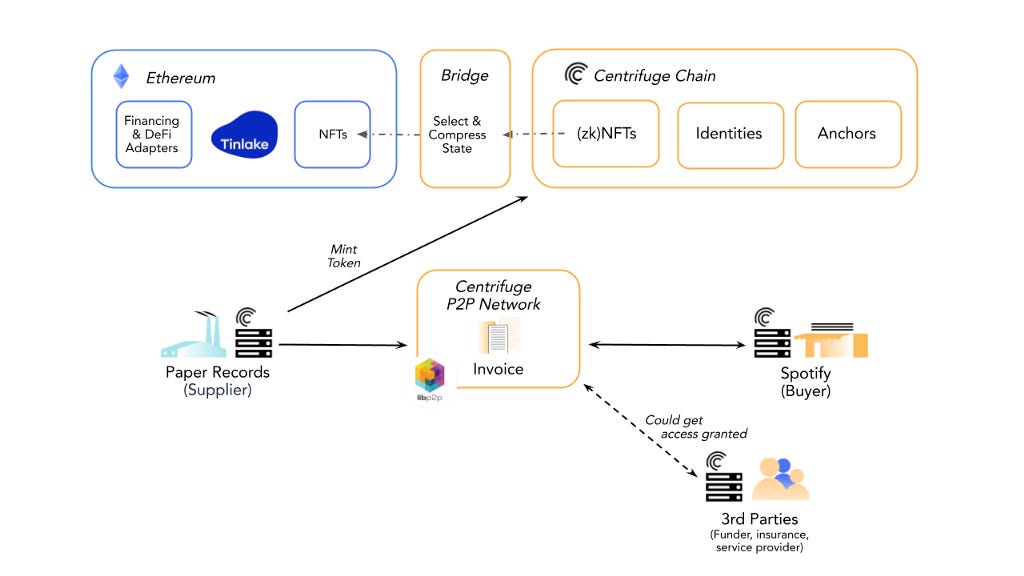

Before we can get knee deep in tokenized microloans and decentralized financial inclusion, we need to understand two resources that will help make this possible — The Centrifuge blockchain, and the Tinlake dApp.

Centrifuge Chain is a Proof-of-Stake blockchain built on Substrate, a blockchain development framework created by Parity Technologies. The Centrifuge blockchain enables users to bring their assets on-chain as non-fungible tokens (NFTs). This is the starting point for originating real-world assets on the blockchain — to begin to unlock financing for any type of asset. This public chain is owned and operated by no single party: the Radial token empowers its holders with governance and provides the incentive for validators to operate the chain.

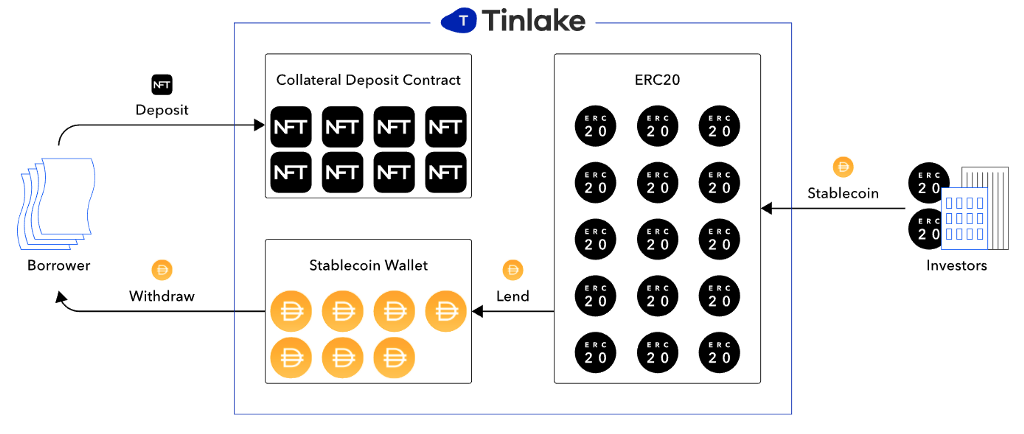

Tinlake, built on the Centrifuge blockchain, allows Asset Originators to finance their assets and Investors to invest in them, all without the trust of a middleman or relying on a single-point-of-failure. Asset Originators can make use of financial tools that are usually only reserved for big corporations: securitizations.

The protocol coordinates the various parties required to structure, administer, and finance collateralized pools of assets categorized by type and risk (IE invoices, mortgages, auto loans, or royalties). By simplifying the process and reducing costs, Tinlake’s protocol creates financing flexibility for Asset Originators, allowing them to optimize risk allocation and access instant funding from DeFi or their traditional investors.

Tinlake’s set of smart contracts pool NFTs that represent non-fungible real-world assets and use them as collateral to finance an asset in a stable cryptocurrency such as DAI or USDC. This is done by issuing fungible, interest-bearing tokens that represent a claim on a fraction of the proceeds of the entire pool. These fungible tokens can be locked in crypto protocols or transferred to investors to draw funding. When liquidity is injected into Tinlake, our risk and yield tokens DROP/TIN are minted accordingly. The same mechanism applies in reverse when funding is paid out and tokens are burned.

Background on Microfinance

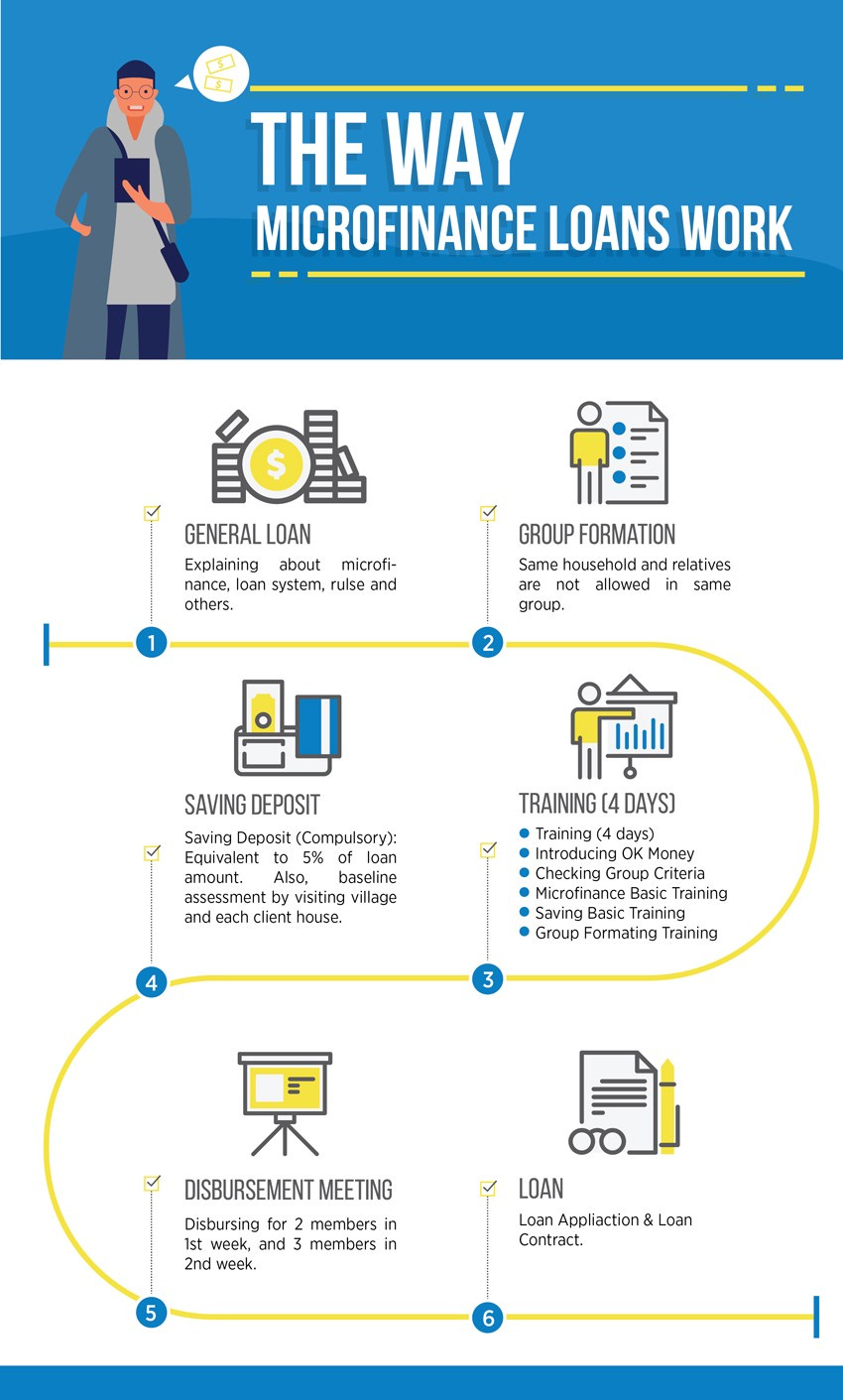

Microfinance is a term used to describe financial services, such as loans, savings, insurance and fund transfers to entrepreneurs, small businesses and individuals who lack access to traditional banking services. Dr. Mohammad Yunus, who is considered the pioneer of modern microfinance, first experimented with making small loans, which he funded himself, to women in Bangladesh making bamboo furniture who had previously relied on loans with unfair and predatory terms to purchase raw materials. He discovered these very tiny loans, which traditional banks did not want to make due to the perceived risks and costs, could make a disproportionate difference to a poor person and given the chance they would pay them back creating a viable business model. He would go on to found Grameen Bank in 1983 and win the Nobel Peace Prize in 2006 (Kiva).

The majority of microfinancing operations occur in developing nations, such as Uganda, Indonesia, Serbia, and Honduras. The World Bank estimates that more than 500 million people have benefited from microfinance-related operations, and, as mobile money systems flourish across international, emerging economies, microfinance products are being cemented as the primary solution for increased financial inclusion around the world (Investopedia).

While some have lauded microfinance as a way to end the cycle of poverty, decrease unemployment, increase earning power, and aid the financially marginalized, some experts say that it may not work as well as it should, even going so far as to say it’s lost its mission. Others argue that microfinance simply makes poverty worse since many borrowers use microloans to pay for basic necessities, or their businesses fail, which only plunges them further into debt (The Balance).

For example, in South Africa, 94% of all microfinance loans are used for consumption, meaning, the funds are used to pay for basic necessities. This means borrowers aren’t generating new income with the initial loan, which means they have to take out another loan to pay off that loan, and so forth and so forth. This translates into a lot more debt. However, other experts say that microfinance can serve as a valuable tool for the financially underserved when used properly. They also cite the industry’s high repayment rate as proof of its effectiveness (The Balance).

Either way, microfinance is an important topic in the financial realm, and if done correctly, could be a powerful tool for many.

Tokenizing Microfinance Loans on Tinlake

So now that we’re familiar with Centrifuge, Tinlake, and microfinance, we can finally discuss the potential of using Tinlake to tokenized microfinance loans and enable social entrepreneurs to potentially crate microfinance institution DAOs!

With Tinlake’s tokenizable invoice feature, microfinance institutions, NGOs and social innovators alike can automate the disbursement of micro-loans with zero liquidity, and quite possibly codify borrower selection requirements via a combination of automated KYC due diligence, scheduled trainings, and smart contracts to greatly simplify the process of attaining the needed loan. The concept makes possible a decentralized investor market for financial products that can create economic change in marginalized communities, without the need for traditional institution support.

Even further, the possibility of micro-lending protocols becomes more of a reality for those that seek to leverage the Tinlake protocol and contextualize its use for customizable micro-lending opportunities. MFIs and NGOs, all of which have specialized approaches to deploying microfinance programs depending on the region their deploying those programs in, would have a much greater capability to more quickly and confidently deploy digital lending products without the capital constraints of funding those loans until they’re paid back by their program participants. Emerging Impact is actively considering trialing this functionality on the Tinlake protocol, and invites MFIs and NGOs to partner with us to responsibly test the possibilities.

Creating a Microfinance Institution DAO (MFI DAO)

If we take the microfinance-by-Tinlake idea even further, we can automate the function of the MFI entity as a whole by creating microfinance institutional DAOs (MFI DAOs). In this scenario, a decentralized network of MFI experts, NGO practitioners, and/or commercial donors could work together through a decentralized autonomous organization to provide micro-loans backed by Tinlake’s tokenized invoice liquidity mechanism. Such a step would exponentially increase access, and decrease bias (particularly racial bias in lending, e.g., in the U.S.).