Blockchain-Based Aid During the COVID-19

Blockchain-Based Aid During the COVID-19

How digital cash aid can support millions during a pandemic.

As the COVID-19 pandemic continues to worsen, many countries are developing economic stimulus packages to avoid a further dive into what seems will be a global recession until a clear vaccine is developed. Provided the minimum 1-year timeline to develop such a vaccine, governments are once again struggling with an ethical and sociopolitical dilemma that has long plagued politicians — “Who gets money and how much?”

Governments around the globe are scrambling to implement economic stimulus programs designed to keep the world economy from sinking into a depression. The price tag to keep the worst from happening — based on what governments have already announced — could grow to more than $10 trillion (Barron’s).

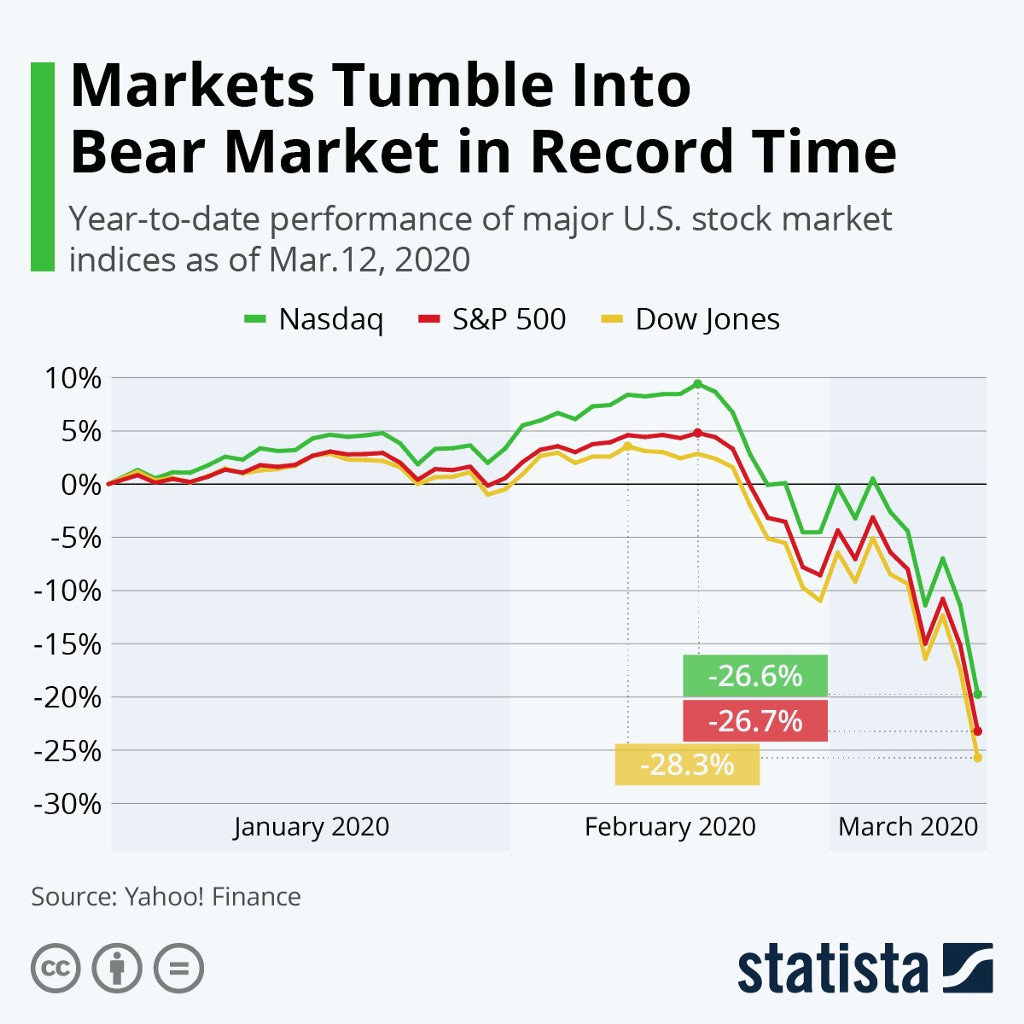

The answer to this question will determine which corporations, particularly in the travel and hospitality industry, cease to exist (or are acquired) and which firms are, once again, too big to fail (i.e. are bailed out). However, unlike the failings of the 2008 recession, it seems that developed nations are more carefully considering which companies get aid, and how they can actually use that aid. As world leaders develop their own answers, the global stock market has plunged into a bear market in only 20 days, a tenth of the time it took for the market to make the same downward movement in 2008, marking the fastest onset of a bear market in history.

In the United States, the Coronavirus Stimulus Bill, which could provide nearly $2 trillion to millions of struggling families and companies alike, is still being debated on the Senate floor. Central to the emerging rescue package is as much as $350 billion for small businesses to keep making payroll while workers are forced to stay home. The package also proposes a one-time rebate of about $1,200 per person, or $3,000 for a family of four, as well as extended unemployment benefits (ABC 7 Chicago).

Urgency is the Key To Saving Lives

The urgency to act is mounting, as jobless claims skyrocket and financial markets are eager for signs that Washington can soften the blow of the health-care crisis and what experts say is a looming recession. In fact, the U.S. Private Sector Job Quality Index estimates that some 37 million domestic jobs are vulnerable to layoffs due the temporary shutdowns created by the viral outbreak (MarketWatch). The figure, of course, is in addition to the 55 million Americans that are unbanked, the nearly 6.5 million Americans that were already unemployed, and the 553 thousand people that are homeless, let alone millions more that are teetering on the edge of economic survival.

The High Cost of Aid

With massive swathes of lower and middle class populations under threat of utility shut-off, housing insecurity, and food insecurity, aid cannot come quickly enough, particularly using traditional financial systems like ACH transfer to each American’s bank account (for those that have one). Some ACH payment providers charge a flat fee, typically ranging from around $0.20 to $1.50 per transaction. Others charge a percentage fee, ranging from around 0.5% to 1.5%. Assuming the minimal fee per transaction at $0.20, the U.S. Government will spend between $47.82 million and $358.65 million of capital reserved for life-saving aid on transaction fees alone (for 128.58 million families and 110.6 million single adult disbursements). Not only that, but in addition to the time it takes politicians to agree who gets what, citizens will need to wait one to four business days to receive the money in their bank account.

For the 55 million Americans that are unbanked, the government will need to spend $3.00 per paper check sent, totaling $165 million in economic aid and increasing the aforementioned cost range to between nearly $50 million and $500 million, representing from 0.25% to 2.5% of the total stimulus package. To put the $500 million upper-range into perspective, that is a third of New York State’s 2014 pre-K education expansion budget, across the state, over the next five years. $300 million went to New York City for the 2014 roll out of the city’s universal pre-K program.

Once the aid is received, even more transaction fees will be taken out for every piece of bread purchased and toilet roll acquired. Beyond the receipt of aid, governments cannot control nor determine how the money is being spent. Families could use the money to bolster their stockpiles just as much as businesses could use it to repurchase their stock. Though the former is as unlikely as the latter is predictable, the sheer extent to how unaccountable governmental aid is is striking. How do we hope to curtail the economic effects of a global pandemic when we can’t ensure out stimulus packages are going to the right resources?

It seems, however we slice it, a great deal of stimulus aid will fall into the hands of non-value added intermediaries and dilute the effectiveness of preventing a global recession.

Digital Cash Aid is Better & It’s Here

The same need for fast and accountable aid that will shape how millions of people survive the economic effects of the pandemic is a problem the humanitarian sector has realized over the past few years. Cash aid is far more convenient and helpful to those in need in contrast to non-fungible aid like clothing and water bottles, particularly because people know what they need better than any government or NGO. The issue is that the speed and cost of disbursing cash aid is onerous, and a lot is lost in transit that could be otherwise used to save lives. To be clear — Fiat money moves slow, just as we thought gold was heavy in 1800.

The use of digital money, stablecoins in particular, could solve this problem in both a conservative, yet innovative manner. Stablecoins are a form of cryptocurrency (no, not the kind used on the dark web to order hits on people) that are non-volatile. In most cases, stablecoins are pegged to the U.S. dollar and use the dollar as collateral (i.e. for every dollar in a the issuing company’s bank account is a stablecoin made available online). Thus, for simplicity’s sake, think of stablecoins as “digital dollars.” Digital dollars can be sent between consumers in mere seconds, and, because they are built on blockchains, there’s always an immutable reference of the transaction taking place. Of course, in order to receive and send digital currency, you need a digital wallet — and these have not been historically easy to use for mainstream consumers.

So how would ordinary people, those who are not accustomed to the world of cryptocurrency wallets and digital asset exchanges, even begin to receive their aid via stablecoins? Wouldn’t the transfer speed and transparency of digital money be made worthless if no one can actually use them?

The good news is that blockchain application user experience has gotten much better, and much more adaptable to the needs of marginalized communities who may not have access to the latest iPhone or laptop. Applications like Sempo, built for digital cash transfer in some of the most remote regions, have already been tested to disburse tens of thousands of dollars at a time to hundreds of people in minutes at a near negligible cost. Used by both the Red Cross, Oxfam, and over 8,000 beneficiaries, Sempo is used to transfer digital money via SMS, Android application, or NFC card instantaneously. The application is built with marginalized community members in mind, and has already piloted in Syria, Greece, Vanuatu, Kenya, and Australia.

Even further, the digital cash being sent can resemble the consumer’s local currency, to avoid any confusion of how much is being received or sent. In this way, those who are unbanked can easily receive aid from their local governments with as much as a cell phone number. Said aid could then be reserved for usage with select vendor partners, like grocery stores, hospitals, and pharmacies, whereas other, non-approved vendors like casinos, liquor stores, and lotteries would be unusable. Once a vendor receives the digital aid from transacting with an aid recipient, the vendor can easily convert the digital money back to cash with the issuing locality or participating aid banking partners.

<a href="https://medium.com/media/ced1a33ceefa8218eafe933a69278ebf/href">https://medium.com/media/ced1a33ceefa8218eafe933a69278ebf/href</a>

Additionally, issuers, like local and federal governments, can receive real-time, anonymized insight from Sempo’s analytics dashboard as to what resources the money is being used for. Such insight can further prepare localities and vendor partners to have stock of the right resources, rather than wasting capital on things people don’t need during a time of recession.

With the use of digital cash aid via blockchain applications like Sempo, we may have an emerging technology tool to help in the cost-effective, fast, and transparent disbursement of economic aid to the world’s most vulnerable communities during the COVID-19 pandemic. By collaborating with local and federal governments alike more people may be able to get the lifeline that they need in time enough to prevent further suffering, and thus, hopefully, further macroeconomic downturn.