Strategic Value in a Capitalistic World

Strategic Value in a Capitalistic World

The benefits of investing in strategic value over a deal value mindset

The benefits of investing in strategic value over a deal value mindset

Sustainable economic value creation is vital for a business to survive. To create value, the company must understand what economic advantages it has and accordingly make and implement decisions that ensure a level of profitability that exceeds the cost of the resources used. This underscores the relationship between strategy and economic value creation, however it is not an easy thing to measure in practice (IE Corporate Relations).

For businesses not necessarily focused on social impact or the social sector (one is not the other), the ultimate goal is to execute opportunities with the greatest total value, a sum of both deal value, or the amount that a contract earns in revenue, and “strategic value.”

Total Value = Deal Value + Strategic Value

To feed corporate growth and ensure that an organization continues to have operational runway, many business strategists will focus on their organization’s immediate pipeline for the fiscal year. Doing so makes sense, and ensures that sales and delivery teams are accountable to a certain level of performance.

However, total pipeline value cannot be equivocated to the sum of total, potential deal value across the engagements in an organization’s pipeline. If teams equate their total potential deal value, that is the total potential revenue earned from commercial contracts in their pipeline, to their total pipeline value, the lower revenue opportunities that provide higher strategic value fall to the wayside.

Total Value ≠ Deal Value

So what is ‘strategic value?’ Strategic Value is the potential amount of capital, whether measured in brand exposure or future potential deal value (in cash or equity), that an engagement can provide. For example, the Advertising Value Equivalency (AVE)resulting from the press release and or media coverage a project generates could also be considered a part of that project’s total strategic value. Each of these opportunities offer much more strategic value than they do deal value, but they’re typically not prioritized by businesses who equate deal value to total value.

A strategically valuable engagement, typically, falls into one of the following categories:

Socially Impactful Projects— Commercial engagements that have relatively low deal value, but tend to create powerfully resonant stories because they hope to affect positive change to the communities around them. These stories are more marketable and can touch a wider variety of potential partners and clients than complex commercial engagements.

Joint Ventures— Commercial engagements that have relatively low deal value, but present the possibility of a joint venture (i.e a startup with a strong product focus) being created from the project. The strategic value is the potential revenue from the joint venture and its equity value.

Governmental Contracts — Commercial engagements in the public sector that have relatively low deal value and long lead times, but present the possibility of an extended contract over a period of 5–10 years and provide significant brand exposure.

Nonprofit Partnerships — Partnerships with nonprofit organizations that motivate your employee base to engage in community service and or leverage your product/service in the context of social impact. These engagements have zero deal value and oftentimes require the corporate partner to sponsor the nonprofit (matching donations, events, etc.)

This is not to say that high deal value engagements do not demand a certain level of strategic value, but they do typically assign more intellectual property to the client, who, depending on the vision of the project, can end the commercial engagement upon the delivery of the project and pursue their own story-telling and or joint venture initiatives. The aforementioned strategic-value use cases, in practice, tend to have socially impactful implications in either the public sector (public services, etc.) or the broader social sector (NGO work, etc.).

Overall, this brief emphasizes the importance of strategically valuable initiatives in organizations that over-prioritize deal value engagements, prompting for-profit organizations to

Develop and utilize a strategic value framework in unison with their business selection framework

Prioritize strategic value initiatives and metrics as equal to deal value engagements in a model that seeks to maximize both in each project

In doing so, I believe commercial businesses can

Expose their product and services to clients/partners in a wider variety of markets

Evolve their respective brands more holistically by communicating both the current and potential consumers and clients that the business cares about social impact (i.e a deal value only focus will de-prioritize a company’s focus on social impact and the public sector)

Evolve their workforce culture into a more dynamic community that investigates opportunities by more than just deal value (i.e a deal value only focus will canabalize an multi-generational culture of innovation, diversity, and inclusion)

A Matter of Priorities

Prioritization of potential business opportunities is integral to an organization’s survival in the commercial sector. However, there should be a holistic framework developed to determine what type of business is prioritized, because the projects don’t just earn the company revenue, they also have an impact on the growth of your employee base, the market’s perception of your company’s strategic focus, and the public’s opinion on what your business values.

Prioritizing one thing will result in the de-prioritization of another thing.

There are four undeniable implications of prioritization as a process:

Prioritizing one thing will result in the de-prioritization of another thing.

There’s a direct correlation to the prioritization level of an initiative and the amount of resources an initiative has access to.

Lower priority initiatives will need to struggle between each other for the remaining amount of resources.

Increased tension around resource allocation will increase organizational politics. Organizational politics decreases operational efficiency.

For example, if your company prioritizes five goals, there will most likely be an uneven distribution of resources in favor of the top two goals. The bottom three goals will need to struggle for the remaining resources, and thus, their respective business leads will compete against each other. Internal competition is the fodder for both increased excellence and organizational politics. An improper and unhealthy balance of resource competition could lead to more dysfunctionality than corporate benefit.

In addition, if the sub-focuses of the top two priorities go unchecked, your business could be spending money on things that are tangential to the focus at hand, and are in fact less strategically important than the efforts of lower prioritized goals. The most common example of business expenses that relate to top-priority goals like revenue generation is the participation in enterprise conferences. Booths at an enterprise summit, in addition to speaking fees, can cost anywhere from $100K to $1M. If your company hopes to engage in all major conferences over the course of a fiscal year, your expenses could be in the millions for conference attendance alone. Do conferences have more strategic value than social impact projects or diversity and inclusion efforts? Which effort has a higher probability of securing deal value later down the road? We’ll get into that later.

The four aforementioned implications of business prioritization can lead us to one succinct, corollary statement

The level of quality of a business’s prioritization process will pre-determine that business’s operational efficiency and thus serve as the predominant influence on the company’s workforce culture and brand perception.

A Framework for Evaluating ‘Strategic Revenue’

To the earlier questions: Do conferences have more strategic value than social impact projects or diversity and inclusion efforts? Which effort has a higher probability of securing deal value later down the road?

The core issue with comparing strategic-value initiatives is the quantification of their respective economic value, particularly when the efforts being compared are categorically different (i.e. a conference keynote speech vs. a project with a social enterprise). One tool that could help create an ‘apples to apples’ comparison framework is what’s used for deal value analysis.

Dynamically Discounted Cash Flows (DDCF)

Dynamic discounter cash flows (DCF) are a traditional method of measuring economic value, but they do not fully quantify the value contributed by a strategic decision. In order to determine the economic value of a strategic decision or effort, we must know what the actual cash flow is in terms of the amount and time period (lead time). For strategic ventures in the context of a DCF analysis, we can leverage (and evaluate) the effort’s forecasted outcomes and map the deal value of each of those outcomes and map their respective probabilities to a cash flow template. This potential for action is called “operational flexibility” (IE Corporate Relations).

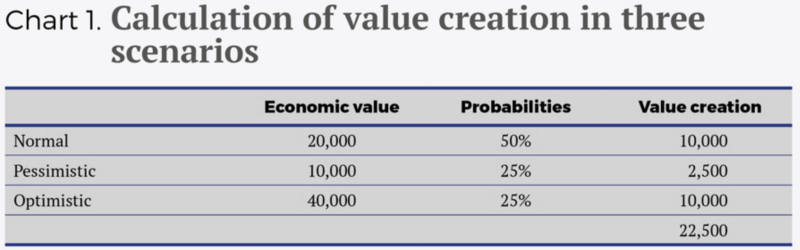

In this case, the traditional DCF becomes dynamic since it factors in the probabilities of possible scenarios occurring. This is best illustrated with an example of investment analysis on a future project (see Chart 1), which reflects three possible scenarios of business development: Normal, optimistic and pessimistic. Every one of these would generate economic value, but they all have different probabilities, so the weighted average economic value would be 22,500 monetary units (IE Corporate Relations).

As such, it is crucial to evaluate not only the business decisions themselves, but also the model for quantifying their impact on value creation. Still, before running the numbers there are some key questions every organization must ask prior to undertaking any major project, regarding the real options of that project and whether they will have value in the future.

For example: Let’s say, that one of our top priorities, as a technology company, is to maximize revenue generation. Given this priority, we have prioritized sub-focuses that the business should hold in an effort to accomplish our goal. Our sub-focuses are:

Support Sales & Delivery: Support aspects of the business that generate revenue (i.e. sell services and or products)

Maximize Enterprise Marketing: Ensure our marketing efforts highlight the solutions we can provide our targeted customers

Participate in Venture Capital: Diversify the companies assets to increase corporate equity value

Hire and Keep the Right People: Ensure the company hires and keeps effective community members to maximize operational efficiency and company performance

Encourage Intraprenuership: Encourage employees to find meaning in their work by adopting their ideas and transforming the best of those ideas into operational, product, or service offerings

Each of these sub-focuses is in a prioritized order that many businesses utilize. Revenue generating parts of the business tend to have the largest budgets, followed by marketing, strategy/investment arms of the business, and then down the line to HR and so on. Our company is faced with a plethora of diverse budgetary decisions:

To send a dozen of our business leaders to Davos and have a booth at the summit

To invest into a flagship, nonprofit partnership

To invest into a flagship, social enterprise engagement in an untapped market. The contract revenue will only be $20K

Each decision results in little or no immediate deal value. Using our DDCF methodology, we can determine the cash value of each strategic decision:

Attending Davos

There are many value considerations when attending an event, but let’s simplify the analysis to expenses and potential revenue.

Expenses

If we want to send 15 corporate representatives and have a booth at the event, we can calculate our costs like so: ($628,000 Strategic Partner Fee, since we’re inviting 5+ people) + (12 People * $19,000 per ticket) + (12 People * 5 Nights Stay * $600 Lodging/Food per Night) + ($140,000 Corporate Lounge/Booth) = $1,032,000.00. Note that these figures are based on informed estimates of the event, and don’t take into account additional costs that provide for VIP access at the event.

Potential Revenue

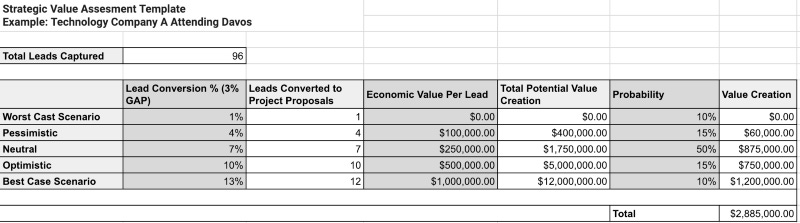

Many of the worlds corporate and state leaders attend Davos. Each of these individuals drive budgetary decisions across their organizations, meaning that, across all of Davos’ attendees, there is most like multiple billions of dollars of budget and net worth in one place. To be candid, cash-strapped clients are good for business. Our team’s goal is to (1) develop as many commercial leads as possible and, (2) convert as many of those leads into pipeline engagements as possible. Let’s start making some reasonable assumptions:

Lead Capture: With 12 people, we can reasonably assume each person will have 1 to 3 meaningful conversations a day with key stakeholders. Meaning that, at the end of the 4-day event, there will be a minimum of 48 leads captured and a maximum of 144 leads captured by all of our representatives. Again, to simplify, we’ll just take the average of the two, or 96 leads

Lead Conversion %: There are many resources online that provide research around average market lead conversion rates. Ideally, your company is tracking is lead conversion performance across events and is leveraging that data to best determine is strategic investments in future events

Potential Value Creation: To provide a secondary gradient, we can also assign a level of economic value with each outcome category: (1) Worst Case Scenario — $0 per lead, (2) Pessimistic — $100K per lead, (3) Neutral — $250K per lead, (4) Optimistic — $500K per lead, (5) Best Case Scenario — $1M+ per lead

Scenario Probability: We must assign reasonable probability of each scenario occurring. I have assigned the following: (1) Worst Case Scenario — 10%, (2) Pessimistic — 15%, (3) Neutral — 50%, (4) Optimistic — 15%, (5) Best Case Scenario — 10%

Combining these measurement attributes, the result should look like the following in Chart 2:

As we can see, the strategic value generated from attending Davos would be $2.9M in potential revenue, or $1.8M in profit given approximately $1M in expenses. If this is either the company’s first year attending Davos, or the company has a proven lead conversion track record from attending in the past, it does make economic since to attend. However, the mere cost of attendance takes a great deal of liquid capital from other potentially lower-cost and higher strategic value initiatives.

A Matter of Corporate Values

At the end of the day, when total value has been calculated across competing interests a company is entertaining, corporate values serves as a guiding force of what is most important. In a world where investors and consumers alike are becoming more conscious about the need for businesses to generate just as much social value as they do for their primary stakeholders, companies will need to make a decision as to what they find important — and such a decision will serve as a market signal to potential clients in the future.