The End of the Yield Greed Era

The End of the Yield Greed Era

The last 13 years of crypto have spanned 4 distinct eras, and the last was colored in greed and systemic collapse. How will these trends affect the next decade of crypto?

The blockchain industry is barely 13 years old but has become one of the world's fastest-growing industries. It has undergone significant changes affecting how people interact with the technology. As the Web3 ecosystem strives for everyday acceptability, it's essential to understand how its evolving as political, economic, and philosophical expectations attempt to find harmony. I posit that the blockchain ecosystem has progressed through three distinct eras - each of which has been the basis for exponential growth - either through increased market capitalization or lesson-learning collapse.

Note, that these eras are defined in the context of blockchain technology maturing as a mainstream technology, as everything continues to evolve in parallel.

Article TLDR

Excessive token emissions only attract fleeting liquidity provision and unprofitable cryptoeconomics

Unscrupulous venture capital protocol investment will continue to encourage the importance of token price manipulation over protocol pragmatism / practicality

DeFi and CeFi collapses (and exploits) will likely provoke regulatory overreaction that further constrains blockchain innovation

Venture capital virtue signaling, nepotistic (i.e., poor) due diligence, and limited crypto-native investment expertise has and will cause artificial, meteoric rises of emerging technology companies that are undeserving of financial support

Protocol pragmatism, token vesting periods, and heightened consumer protection via cybersecurity and education will be the blockchain redeemers of 2023+

The Bitcoin Era (2009 - 2014)

The Bitcoin Era was defined as one that introduced blockchain technology to its first adopters, strengthened a philosophical culture around trustlessness and transparency, and evolved the dynamics of pseudo-anonymous Internet e-commerce. However, every meteoric rise often comes with its failures, and central exchange fraud, paired with illicit use of BTC - then thought to be an anonymous digital currency - introduced the world to a seemingly ‘veiled and sketchy’ crypto-community. Regardless, Bitcoin’s total market capitalization went from ~$16k to $6.7b (a 41,874,900% increase), and its association with e-commerce and exchange collapses actually helped legitimize its usefulness as a trustless, transparent, and most importantly, immutable, digital commodity.

2009: A Star is Born

On January 3, 2009, Bitcoin, the world's first decentralized blockchain and digital currency, was launched. Built to become ‘a purely peer-to-peer version of electronic cash,’ Bitcoin solved a longstanding problem of digital currency - the ability to prevent the expenditure of the same digital currency twice or more to avail the multiple services (a.k.a. ‘double spending’). Originally designed as a store of value with a fixed supply, Bitcoin re-introduced the contagious ethos of trustlessness and third-party disintermediation that was quickly adopted and catalyzed by the cypherpunk community. Bitcoin's launch would be the birth of the blockchain industry.

By October 5, 2009, New Liberty standard (NLS) became the first site to publish an official exchange rate for Bitcoin. The first-ever exchange rate was $1 for 1,309.03 BTC, equivalent to 7.6 cents per 100 bitcoin. It was one of the few sites that allowed people to trade bitcoin using PayPal.

The prevalence of centralized crypto exchanges continued to grow as ‘altcoins,’ or other decentralized digital currencies (often forks of BTC itself) began to flood the market. Mt Gox, for example, was established in 2010. There was no regulation or oversight of most exchanges at this point.

At the same time, the development of crypto meetup forums was on the rise. Digital currencies were unpopular, so Bitcoin enthusiasts needed regular online meetups to discuss how to grow the crypto space. Forums like Bitcointalk and Bitcoin garden were among the first crypto hangouts. Others were launched on various social media platforms, especially Twitter and Reddit.

These crypto meetups brought together enthusiasts, developers, and investors to discuss new ideas. These online meetups were very helpful, as it was during a Bitcointalk forum that the founder of New Liberty Standard suggested the adoption of the bitcoin symbol and ticker we use today.

The Fall of Silk Road

Silk Road was a digital black market platform that was popular for hosting money laundering activities and illegal drug transactions using Bitcoin. Founded in 2011, the Silk Road was born out of a need to connect illegal drug sellers with interested buyers online while protecting their identities and transactions using anonymization techniques. All trades on the Silk Road were conducted using BTC (i.e., bitcoin). Some analysts estimated that only four percent of bitcoin transactions were dedicated to the Silk Road.

The Silk Road came to its demise in 2013 after the FBI learned about the existence of the hidden marketplace and colluded with the DEA, IRS, and Customs agents. Although the federal agents admitted that the use of Tor and Bitcoin to obscure addresses were major obstacles that they encountered, they were still able to crack down on the underground drug market. The FBI shut down the site permanently, seized more than 144,000 bitcoins (then valued at $34 million, but valued at $2.4 billion at the time of this writing), and arrested a number of users of the site including the founder, Ross Ulbricht (a.k.a. “Dread Pirate Roberts,” or “DPR” on Silk Road), who made about $80 million in commissions from transactions carried out within the site. Ulbricht was convicted in 2015 and is currently serving a life sentence without the possibility of parole.

Interestingly, in the FBI complaint against Ulbricht, the agency stated that “bitcoins are not illegal in and of themselves and have known legitimate uses,” a strong statement about the legality of bitcoin. The arrest of DPR may have helped remove the association between bitcoin and crime, as bitcoin was revealed to be a less than perfect currency for criminals. The immutable ledger or blockchain, provides a record of every transaction. This enabled law enforcement to track illegal transactions, despite the lack of a name or bank account attached to bitcoin addresses.

The Fall of Mt. Gox

Mt. Gox exchange, launched in 2010, was handling about 70% of all bitcoin transactions at its peak. The exchange had experienced some technical issues over the years, but nothing prepared the founders for what happened in 2014.

Mt. Gox was attacked by unknown hackers who withdrew about $460 million worth of bitcoin. This greatly affected the exchange, as the first thing users noticed was the inability to withdraw funds. In a few days, the exchange suspended all trading and went offline. While the total number of bitcoin stolen that day is largely disputed, it is estimated to be about 744,408 Bitcoins. The company filed for bankruptcy a few weeks after failing to retrieve all coins.

The only upside to Mt. Gox's downfall was the increased focus on the security of crypto exchanges which led to the implementation of regulatory policies like Know Your Customer (KYC) and Anti-Money Laundering (AML) on crypto companies. A significant step in increasing public trust in cryptocurrencies. But cryptocurrencies were still a long way from widespread public confidence.

The collapses of the Silk Road and Mt. Gox, paired with the emergence of Ethereum generalizing blockchain technology to support applications beyond peer-to-peer transfer marked the end of the crypto-community’s first mainstream era - The Bitcoin Era. To many mainstream consumers, the term “Bitcoin” would continue to represent the blockchain and cryptocurrency ecosystem as a whole.

The BUIDL & HODL Era (2014 - 2018)

The collapse of Silk Road and Mt. Gox formerly introduced Bitcoin to mainstream consumers. As an increasing number of alt-coins and centralized exchanges (CEXs) entered the market, there was one thing missing to take blockchain technology to the next level - generalized use-case applicability and ease of development. The Ethereum blockchain introduced such capabilities and laid the foundation for the multi-use case blockchain ecosystem as we know it today, inspiring a new developer class - so-called “Blockchain Engineers,” to create decentralized applications of the future (i.e., “dApps”).

Ethereum (2015+)

The next significant era in the evolution of the blockchain ecosystem is the advent of Ethereum – a bitcoin-like blockchain that could host decentralized apps (dApps). Bitcoin was strictly limited to peer-to-peer financial transactions, and it was very difficult to build Bitcoin-based applications at the time. In 2013, this led a Canadian developer, Vitalik Buterin, to propose a new platform which would allow to apply the trustlessness, immutability, and transparency of blockchain technology to virtually any use case in the form of ‘decentralized applications,’ or ‘dApps.’ The platform, named Ethereum, would become the foundation for use-case driven blockchain technology globally.

Unlike Bitcoin, Ethereum apps would rely on smart contracts, which are if-yes commands that execute set instructions when certain conditions are met. Smart contracts process peer-to-peer transactions without intermediaries like a bank or payment company. To incentivize computers to contribute transaction processing resources to the network, the Ether token (i.e., “$ETH”) is rewarded using the Proof-of-Work consensus model (now proof-of-stake).

In 2015, following an initial fundraiser, Ethereum was launched and 72 million coins were minted, marking the world’s first ‘Initial Token Offering’ or ‘ICO.’ $ETH) ICO price was roughly $0.31. The price of the Ether token gradually increased during the ICO, from 2,000 ETH for 1 BTC to 1,337 ETH for 1 BTC. The minimum amount for participation was 0.01 BTC. Ethereum’s smart contract SDK for Solidity, Ethereum’s native smart contract programming language, would then be used to develop the world’s first decentralized applications and protocols.

The DAO Hack (2016)

As developers began mapping the capabilities of smart contracts and real-life use cases, one of the first dApps was “The DAO,” The DAO allowed users to join a community of investors who pool together funds to be invested in projects voted on by community members (i.e. a decentralized kickstarter for crowdsourced investment, where no single entity owns the investment vehicle).

The DAO was met with immediate success, yet on June 17, 2016, The DAO was hacked by a developer who identified a smart contract exploit which allowed them to steal 3.6 million ETH (i.e., $70M in $ETH at the time). To refund the lost money, Ethereum hard-forked (created a new Ethereum blockchain that eliminated the exploit transaction from its history) to send the hacked funds to an account available to the original owners. The token owners were given an exchange rate of 1 ETH to 100 DAO tokens, the same rate as the initial offering.

Even worse, the United States Securities and Exchange Commission (SEC) released a ruling following The DAO hack on July 25, 2017 that stated:

“Tokens offered and sold by a “virtual” organization known as “The DAO” were securities and therefore subject to the federal securities laws. The Report confirms that issuers of the distributed ledger or blockchain technology-based securities must register offers and sales of such securities unless a valid exemption applies. Those participating in unregistered offerings also may be liable for violations of the securities laws.”

In other words, The DAO’s offering was subject to the same regulatory principles of companies undergoing the initial public offering process. According to the SEC, The DAO violated federal securities laws, along with all of its investors (Falkon).

The DAO hack served as two hard lessons for the blockchain community: (1) smart contract cybersecurity carries exponentially more risk than that of traditional programs because of their ability to move and custody digital money directly, and (2) just because cryptocurrencies were a new asset class, they could still be considered securities by regulatory authorities. Such considerations would be recurring lessons as the blockchain ecosystem continued to expand.

The Age of ICOs (2017 - 2018)

As the Ethereum developer community grew, the world’s first dApps and protocols gradually came into existence and Web3’s first entrepreneurs began to understand how best to apply blockchain technology to a myriad of problems plaguing today’s traditional-finance markets. To fund their projects, many startups created project-based tokens (i.e., cryptocurrencies) that could be used for the community to govern their decentralized applications and exclusively access other rewards and functions of their solution. Founding team’s would sell a portion of these tokens in an effort to crowdsource funding - a practice that was referred to as token sales, “Initial Token Offerings,” or “Initial Coin Offerings” (i.e., “ICOs”).

Many projects launched their fundraising efforts via ICOs long before they started actual development. Rather, founding teams published “white papers” providing a research-based brief of their solution, total addressable market, and, oftentimes, project token distribution. Over the course of 2017 to 2019, ICOs raised an estimated $4.9 billion. The budding blockchain ecosystem’s exponentially increasing need to fund greenfield innovation via ICOs invited venture capital into the process of Web3 startup financing, further familiarizing the technology with mainstream interest and investment.

The nature of ICOs gradually transitioned from public offerings to private offerings (i.e., with accredited investors and venture capital firms) as Web3 teams sought to avoid regulatory oversight and having their tokens labeled as securities. VC firms began to make “equity + token” deals that, when paired with marketing capital, could generate an almost immediate investment ROI because of the liquidity and secondary market demand of the portfolio project’s token. Finally, as nearly 1,000 cryptocurrencies entered the secondary market from 2016 to 2018, with their release fueled by landing page marketing, fundraise press releases, and VC-investment signaling, many retail investors realized massive investment gains from ‘HODLing” (i.e., holding) on to their tokens.

The Crypto Greed Era (2018 - 2022)

The public and private ICOs of 2017 and 2018 solidified venture capital support of the blockchain ecosystem - which was quickly evolving into a corporatized industry as incumbents such as Amazon and IBM began to provide their own blockchain solutions. VCs went on to invest more than $25 billion in blockchain companies in 2021, and then a further $16 billion in the first six months of 2022, according to data from CB Insights. Retail investors helped contribute upwards of $10 billion in total value locked (TVL) across blockchain’s largest DeFi protocols in exchange for the promise of extraordinarily high APYs (> 100%). More so, technical entrepreneurs flood decentralized exchange protocols with high-frequency trading bots to create the arbitrage foundation that the ecosystem’s liquidity relies upon today. The greed of crypto quickly eclipsed its innovative and cypherpunk origins only to conclude in spectacular collapse that now threatens a reaction of regulatory overreach.

Private Token Sales & Token Warrants (2018 - 2022)

As the SEC began to hand out subpoenas to blockchain startups that benefited from the 2017-2018 ICO-mania, public token sales fell out of style and private token sales directly to accredited investors took its place. Private ICOs of pre-built projects promised investors immediate, low-risk ROIs as decentralized and centralized cryptocurrency exchanges accrued liquidity at an exponential rate in the amount of tens of billions of dollars. Such token sales were/are executed using token warrant and are often executed in parallel to an equity investment - promising the investor a certain allocation of tokens at a pre-market entry price. Venture capital institutions with enough social or literal capital created token investment and liquidity supply chains between themselves, centralized exchanges, market makers (i.e., OTC trading firms), and their portfolio companies/protocols to virtually mint money. Such practices added thousands of governance tokens (i.e., cryptocurrencies used for supposed protocol governance) to the secondary market through centralized and decentralized exchanges and pump-and-dump schemes and trading attacks quickly ensued.

The World Meets NFTs (2020 - 2021)

Despite NFTs being first introduced in 2014, they didn’t gain mainstream attention until 2020, where NFT sales reached $82.5 million and increased to $17.7 billion in 2021 alone — a jump of more than 200 times.

For background, NFTs, or non-fungible tokens, are unique digital assets that represent non-fungible assets, such as art, game assets (characters, weapons), real estate, etc. The potential of NFTs is to digitize non-fungible assets and exponentially increase their traceability, liquidity, and ease of transfer, which would greatly reduce the operational cost of facilitating traditional, non-fungible asset transactions.

In 2020, NFTs broke into the mainstream in four distinct ways:

NFT DEX Yield - Retail investors could earn yield in a DEX’s (decentralized exchange, in this case, for NFTs) native token in exchange for their platform participation. Users would then sell off this yield to generate income (e.g. Rarible).

NFT Fractionalization - Blue-Chip NFTs of incredible popularity and price, such as Crypto Punks, could now be fractionalized as fungible, ERC-20 tokens. Retail investors could then more easily trade their fractional ownership tokens and reinvest them into liquidity pools to earn additional yield (e.g., NFTX).

NFTs in Gaming - Major gaming brands and up-and-coming Web3 games financialized their in-game assets to become tradable on secondary markets (i.e., NFT trading platforms and DEXs). Gamers could now earn in-game rewards and assets that had easily convertible, secondary market value (i.e., play-to-earn became real for the first time ever) (e.g., Sandbox).

NFT Art - Major and up-and-coming artists alike digitized limited edition artwork on-chain. Oftentimes, these pieces came in the form of randomized, character-based series such as Bored Ape Yacht Club, CloneX, and Vee Friends.

Art-based NFTs (i.e., digital collectibles) were at the center of quick-flip-for-profit hype cycles that were worsened by the first widespread celebrity-entry into the blockchain market. Discord quickly became the home of thousands of NFT launch community groups, inviting both novice, NFT retail investors and crypto-scammers into the same Internet dormitories. Over 46,000 people have reported cryptocurrency scams between the beginning of 2021 and March 2022. In that year alone, $680 million was reported lost from crypto scams. Another $329 million has been lost to crypto scams in the first three months of 2022. Crypto-native consumers participated in the NFT DEX, fractionalization protocol, and gaming-focused part of the market - all which benefited greatly from the ballooning NFT art-market.

As with all market bubbles, collapse was inevitable as the FY22 trading volume of NFTs plummeted from its peak of $17 billion in January to $466 million in September — a staggering 97% drop. Not surprisingly, the many unsophisticated retail investors that made NFT trading volumes extraordinarily high became the victims of the market’s collapse, or of outright fraud sullying most Discord channels.

Infinite Yield Protocols (2020 - 2022)

DeFi started off as an incredibly broad term; a catch-all reference to any novel financial project powered by crypto. But in June, DeFi centered around one thing: That’s when , a DeFi lending protocol, issued $COMP tokens to anyone who used it. Within a few days, $COMP was so valuable that people started taking out loans purely to farm the token. Other protocols followed suit and the summer of DeFi began (Decrypt).

Protocols began offering yield APYs of upwards of 1,000%, battling for liquidity to be staked within their smart contracts to boost the secondary market value of their respective governance tokens. From April 2021 to April 2022, DeFi protocol yield attracted an ecosystem high of $248 billion in TVL (total value locked).

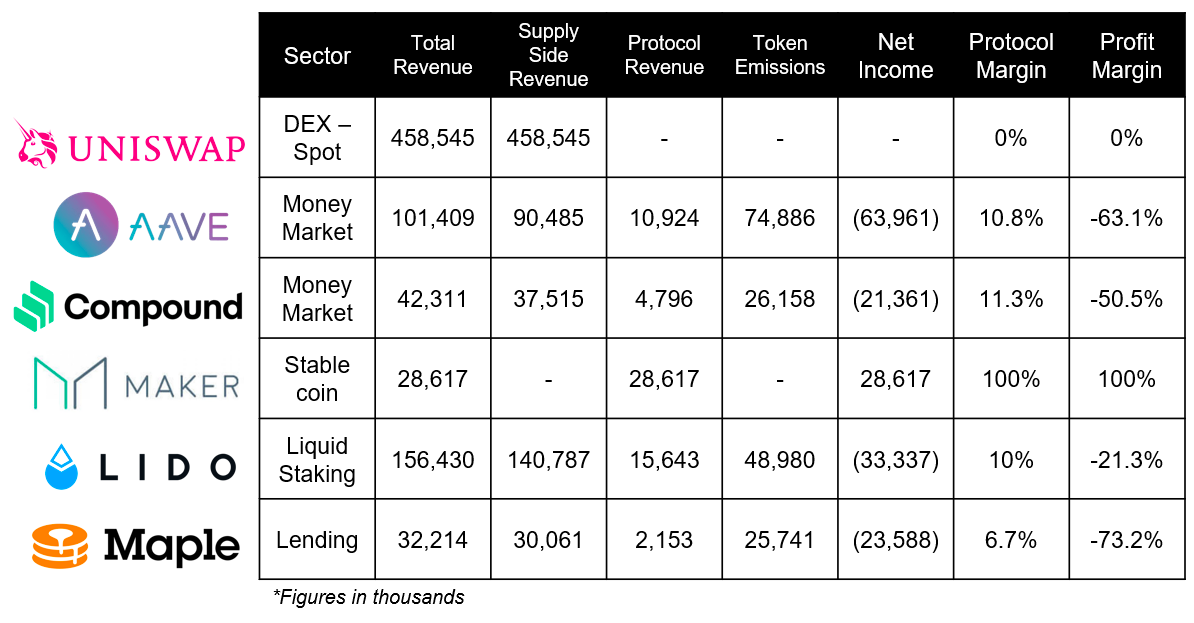

However, such yield are (and continue to be) systemically unsustainable for two reasons: (1) liquidity provider desire for governance token yield is predicated on the existence of a healthy, upsurging secondary market so that token-flipping is possible, and (2) token emissions used to create high yields put a strangle-hold on a protocol’s unit economics, making it impossible for them to become profitable (and thus self-sustaining). In fact, token emissions remain one of the primary reasons for the lack of profitability in DeFi.

SEBA, a regulated crypto bank in Switzerland, hit the nail on the head when it released a report commenting, “Yield farmers made money by hopping from one protocol to another. As long as there are buyers for new protocol tokens, yield farmers can continue jumping among protocols. When buyers stop accepting the other side of the trade, this deranged activity will be arrested. Clearly, this trend is not sustainable.”

Since the crypto market’s collapse in the latter quarters of 2022, global DeFi TVL has fallen $77 billion, a nearly 69% decrease in less than six months. The yield maximization trend not only led to the collapse of several, multi-million dollar protocols, but it also redefined the purpose of ‘staking,’ which originally was used to either (a) further economically secure a protocol or network from additional risk related to its function (e.g. lending) or (b) served as a disincentive not to cheat the protocol or network’s operating rules.

Systemic Protocol & CEX Collapse (2022)

2022 saw the beginning of the end of the Crypto Greed Era. NFT sales and cryptocurrency prices dropped precipitously, overall DeFi TVL declined by over 60%, and protocol profit margins worsened YoY. The nail in the coffin where major CeFi (Centralized Finance) and DeFi market collapses that will undoubtedly provoke the backhand of regulators. The most infamous cases were the collapse of the Terra protocol and the FTX exchange - both which contributed toward the secondary market’s price collapse as retail investors retreated from cryptocurrency altogether back to their native fiat.

Terra Luna Collapse (May 2022)

Terra is a blockchain network, or Bitcoin, that produces Luna tokens. The network was created in 2018 by Do Kwon and Daniel Shin of Terraform Labs. Terraform Labs created the UST coin to be an algorithmic stablecoin on the Terra network. While other stablecoins (USDC or Tether) are fiat-backed, the UST would not be backed by real assets. Instead, the value of UST would be backed by its sister token, Luna (Forbes).

Luna was Terra’s blockchain native token, similar to how ether is used on the Ethereum network. The largest incentive was that you could stake your UST holdings on the Anchor lending platform for a 20% annual yield. Many analysts felt that this absurd rate was unsustainable (Forbes). At one point, as much as 72% of UST was deposited in Anchor because the platform was the primary driver of demand for Terra.

On May 7, 2022 over $2 billion worth of UST was un-staked (taken off the Anchor Protocol), and hundreds of millions of it were quickly liquidated. There’s debate as to whether this happened as a response to rising interest rates or if it was a malicious attack on the Terra blockchain. The huge sell-offs brought down the price of UST to $0.91, from $1. As a result, traders started to change 90 cents worth of UST for $1 of Luna. Once a large amount of UST had been offloaded, the stablecoin started to depeg. In a panic, more people sold off UST, which led to the minting of more Luna and an increase in the circulating supply of Luna (Forbes).

Following this crash, crypto exchanges started to delist Luna and UST pairings. Long story short, Luna was abandoned as it became worthless (Forbes). It’s estimated that the Luna crash ended up tanking the price of bitcoin and causing an estimated loss of $300 billion in value across the entire cryptocurrency space. It’s estimated that about 280,000 people in South Korea had invested money in Luna.

FTX Collapse (November 2022)

FTX, a crypto exchange, went from being worth $32 billion to filing for bankruptcy in what many are calling the “Lehman Brothers Moment” for crypto. Sam Bankman-Fried, often referred to as SBF, is the 30-year-old founder of FTX, the crypto exchange. He amassed a net worth of $26.5 billion at the peak of his wealth (Forbes).

SBF also cofounded Alameda Research, a crypto hedge fund named after his hometown, in late 2017. SBF then created his own crypto exchange, FTX, in 2019 based on the success of Alameda. The exchange grew fast with high-profile acquisitions, a hefty marketing budget, and promises of high returns. Users were told that they could earn much higher yields with FTX than with other traditional banks (Forbes).

Problems around the legitimacy of FTX and Alameda Research began when Coindesk made claims that both firm’s main asset on their balance sheets was FTT, the native FTX network token (much like how Binance has BNB, Ethereum has ETH, etc.), meaning that their corporate assets were tied to a risky and volatile token. Amidst such a realization, Binance, a rival exchange, announced it was going to sell around $530 million worth of FTT. Such a massive liquidation caused the price of FTT tokens to drop as investors rushed to take their money out of FTX, figuring that this would be the next crypto company to collapse. The “CeFi run” on FTX reached an estimated $6 billion, which led to a liquidity crunch for FTX (i.e., FTX didn’t have enough money to fulfill said requests). The $6 billion in withdrawals in 72 hours was enough for FTX to pause withdrawals. FTX shortly filed for bankruptcy for it and all its subsidiaries, and SBF was subsequently arrested in The Bahamas and then later let out on bail for $250 million.

During FTX’s fraudulent stint, it’s important to note the role that venture capital played in its meteoric ascent. SBF raised more than $1.8 billion from investors, many of which conducted poor due diligence on the merit of institutional virtue signaling from incumbent firms. The fundraised capital was subsequently spent on multibillion dollar marketing campaigns, political campaign donations, celebrity endorsements, and the purchase of real estate for FTX executives (and even SBF’s own parents). FTX’s income statement and balance sheet were in tatters and their overall financial management was one of the most mismanaged departments in corporate history. John Ray III, the lawyer who was hired to oversee the liquidation of Enron and now the FTX cleanup, remarked, “I have over 40 years of legal and restructuring experience. I have been the chief restructuring officer or chief executive officer in several of the largest corporate failures in history. . . . Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.”

The collapse, which was the result of CeFi (centralized finance) fraud (to be crystal clear), triggered a slide in cryptocurrency prices that wiped out some $183 billion of value from digital assets in November 2022. The collapse has also worsened the blockchain ecosystem’s regulatory front, with several state and federal agencies launching or expanding investigations into FTX, including the U.S. Department of Justice, the U.S. Securities and Exchange Commission, the Securities Commission of the Bahamas and the Bahamas’ Financial Crimes Investigation Branch. Calls for better consumer protection are being made that, depending on the extent to which they are implemented, could undo the legality of true DeFi as we know it.

Pragmatic Defi Era and Beyond (2023+)

Despite over $400 billion being wiped from the crypto market in 2022 alone and a high likelihood that oncoming, American regulation will threaten the censorship resistance and decentralization of blockchain protocols, the end of the Yield Greed Era does carry a great deal of opportunity. 2023 marks the beginning of a new chapter focused on

developing pragmatic, risk-oriented protocols, and;

finding a reasonable path forward for the co-existence of consumer protection, national security, financial compliance, and the core tenants of decentralized finance.

Already, protocols such as Goldfinch and Maple Finance are quickly setting the foundation of “real-DeFi,” where real, everyday businesses and consumers can leverage DeFi protocols to lower the cost of accessing financial services in a compliant manner. Just like the BUILD & HODL Era that championed ICOs, many of the companies that will survive the Crypto Greed Era will be ones that are focused on solving real problems, rather than maximizing yield APYs or flipping the next, popular NFT. There are more collapses to come, but for everyone the blockchain ecosystem becomes better for it.